Blockchain Briefs: Sui

An introduction to Sui and an exploration of its growing ecosystem.

Disclaimer: Any content and resources I provide is for the purpose of education, entertainment and general information and use only. Nothing I say should be construed as legal, financial, investment, tax or other advice or information. I am not an accountant or financial advisor and I do not hold myself out to be. Any data provided is given at the time of writing only.

Welcome! “Blockchain Briefs” is my article series exploring different blockchains, protocols, applications, or other projects and trends within the blockchain / crypto industry. These articles are intended to be simple overviews with sprinkles of personal commentary, rather than exhaustive technical research papers. I aim to base most of what I say on verifiable facts and data. However, some of my opinions may rely more on an instinctual feel or perception. Why? Because crypto is one of the most nascent and freest markets in the world and remains heavily influenced by emotive narratives, which should not be ignored.

For my first article, I will be looking at Sui.

Apparently there was a bit of a dramedy about Sui #grant posts in the past month. Well, I can promise you this article is not grant related at all - I’m clearly not anything close to an influencer.

I believe it is a good time to review Sui (and many other ecosystems) as we move through Q3 and the market has had almost half a year to digest the hype and explosive growth in prices and users that occurred throughout Q4 2023 - Q2 2024.

Introduction

Before I discuss Sui, I want to give a bit of context to the overall Layer 1 landscape.

There has been no shortage of Layer 1s or “Alt-L1s” that have launched since Ethereum went live in 2015. While I think it should be clear that Solana is firmly on the path to establishing itself as the #3 chain behind Bitcoin and Ethereum,1 few other Layer 1s can convincingly claim to have maintained comparable relevance across multiple market cycles or a competitive level of developers, users, capital and mindshare.2 There are a few interesting projects developing on Avalanche, particularly for gaming (e.g., Gunzilla subnet and Off The Grid, Shrapnel), and TON (The Open Network) has seen explosive growth in recent months,3 but those ecosystems need more time to prove that they can sustain and grow themselves in an increasingly competitive market.

Despite Layer 1s having a very low rate of success, developers and investors have not stopped trying to strike gold with the next big Layer 1. These continued attempts are probably partly attributed to the fact that there is now significant consensus that the future will be multi-chain and the industry will be more than big enough to accommodate several major Layer 1s (maybe 4 or 5 or possibly more), each with their own cultures, category focuses and technical pros and cons. This obviously means potentially massive financial upside for the developers and investors who succeed. However, there is much to be said about there already being an over abundance of chains and blockspace. The industry needs to place much greater focus on funding and building meaningful consumer apps rather than more copy-paste infrastructure layers, especially given an underwhelming amount of mainstream consumer adoption of crypto-native apps (or Web2 apps that integrate Web3 elements). That is a topic for another day but throughout 2024 market sentiment has quickly shown increased weariness to continued infrastructure funding (or “infra masturbation” as some have colourfully put it).4 The people want things to do onchain!

The crypto industry is obviously relatively nascent, but at this stage in order for a new Layer 1 to have a real chance at success, it needs to offer something truly unique to differentiate itself from the incumbents. Solana has set a new standard for mass adoption ready blockchains with its ultra low fees and high throughput, so new Layer 1s cannot merely deliver the same. I am paying attention to next generation Layer 1s also offering novel elements. I believe Sui could fit into that category, as well as Monad (Parallel Execution EVM) and Berachain (Proof of Liquidity), both of which plan to launch their mainnets in late 2024 and are leaning heavily into community and memetics to gain mindshare and loyalty.5 Developers and investors slapping together another “EVM-compatible Layer 1” promising low fees and fast TPS (or other buzzwords) is not enough and those are destined for the graveyard as ghost chains.

This leads me to Sui.

What is Sui?

Sui is a next-generation Proof-of-Stake, Layer 1 blockchain with ultra low fees and high throughput that launched its mainnet in May 2023. Prior to mainnet, Mysten Labs, the core developer for Sui, raised $336 million USD in two private rounds and approximately $54.3 million USD in public offerings.

Sui introduced a new blockchain architecture with the Move Virtual Machine (Move VM). This is Sui’s unique element. If we can foresee a multi-chain future, then it should not be far fetched to believe that multiple VMs are part of that future. There have been plenty of analogies to the multiple leading Operating Systems of Apple, Windows, Linux and Android.

I won’t delve deep into the technical aspects of the Move VM or contrast it to the EVM or SVM as that it outside my area of expertise, but a few general points need to be made.

Sui was developed by former Meta employees who were involved in its now abandoned Diem and Novi digital currency projects. Those projects were the open-source foundation for the creation of the original Move programming language which was subsequently adapted for Sui. Sui is not the only blockchain project that spun out of Meta. Aptos is widely considered to be Sui’s immediate competitor as it was also founded by members of Meta’s Diem project and utilises the Move language for Aptos’ version of a Move VM, which is closer to Meta’s original version. This point is important - while Move is generally said to be scalable, more secure and easier to build with than other VMs and languages,6 not all Move languages and VMs are created equal. Sui-Move is different to Aptos-Move as well as Movement Labs’ Move. This brings its own hurdles for Move-based ecosystems - @artoriatech posted interesting criticisms of the Move VM, which I strongly suggest reading as well as the replies from other leading Move developers.

I am not here to compare Sui to Aptos in depth.7 However, I personally favour Sui right now for several reasons: although Sui is around 8 months younger than Aptos (Aptos launched its mainnet in October 2022), Sui has attracted greater inflow of capital into its DeFi ecosystem as well as developers, users and general market mindshare. This could change but for now Sui has more overall momentum.

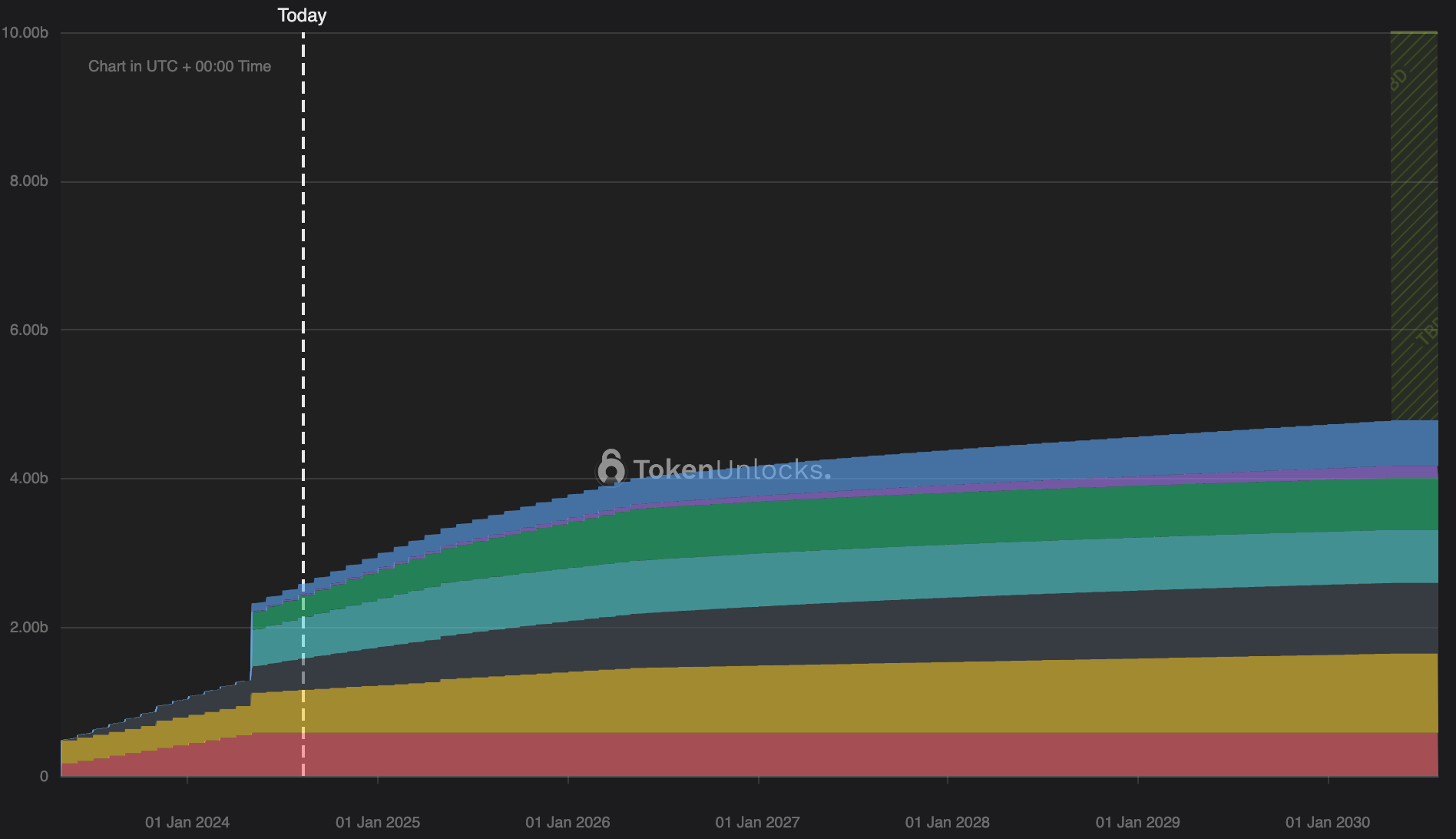

Tokenomics

The economics of Sui’s native currency SUI (or “tokenomics”) are important but you can learn most of what you need to know from sources such as Token Unlocks and SuiVision.

In short, there is a circulating supply of approximately 2.6 billion SUI and a total supply of 10 billion SUI (1 billion SUI is set aside for staking rewards). The market cap/FDV is currently 0.26. A large unlock for early investors and contributors occurred in May 2024. On the face of it this distribution does not look horrible for an early Layer 1 given that long term network incentives through emissions like staking rewards are necessary to assist network growth and adoption.

However, when you dive deeper there are a couple key issues:

First, like many other recent major projects, SUI launched at a comparatively high public valuation where most of the valuation increase was captured in private markets. This is significantly different to how retail investors were able to buy ETH and SOL at low initial public valuations.8 This is important because the success of Bitcoin, Ethereum and Solana led to a “wealth effect” for early retail buyers. That wealth effect cannot be underestimated because those early supporters can become a network’s biggest proponents and help contribute to sticky network effects.

Second, Justin Bons pointed out two important issues in his recent criticisms of SUI’s token economics:

Sui is effectively centralised as the Sui Foundation controls over 5.22 billion SUI that is marked “unallocated” until 2030 and custodied by third party custodians. The Sui Foundation has not provided clear evidence that the unallocated SUI is legally locked with the custodians until 2030. It is not locked onchain. This means we essentially have to trust the Sui Foundation, which is antithetical to what should be a trustless system; and

Over 8 billion SUI is staked and around 84% of that staked SUI is controlled by the founders and the Sui Foundation with no locking guarantees. However, the Sui Foundation confirmed in a response to Bons that “100% of staking rewards earned by the Sui Foundation are returned to the community and included in the public emission schedule.”9

Although these economic issues (whether you think they are real or not) will not prevent Sui from being successful, any market distrust that stems from them might slow the adoption of Sui and its native currency. That being said, Sui is not the first major Layer 1 to come under fire for its tokenomics. A few years ago Solana did too. Much of the distrust might be cleared if, for example, the Sui Foundation’s communication becomes clearer and/or in the years to come onchain governance votes for radical, positive changes to SUI’s economic structure.

In addition, unlike APT, ETH, SOL or many other Layer 1 currencies which will continue to inflate, the max supply of SUI is known in advance (10 billion SUI). The potential demand for SUI is not though. It will be interesting to see how that affects investor sentiment if Sui manages to attract more attention.

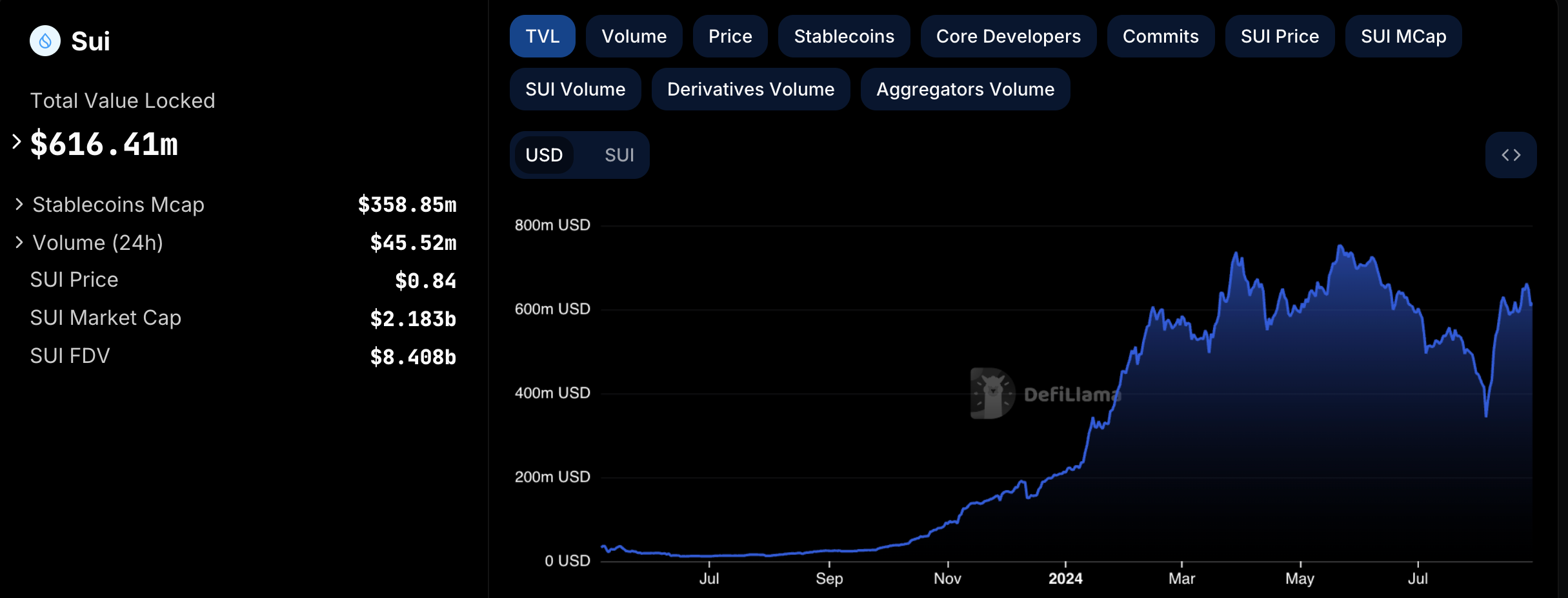

Total Value Locked (TVL)

Total Value Locked (TVL) analysis can be interesting, but I prefer not to focus on it alone. It is a basic metric for measuring a chain’s economic activity, especially in the new era of high-throughput, low fee Layer 1s. TVL was previously regarded as the holy grail of metrics, but its limitation has become more apparent with Solana’s recent achievements. Solana’s transfer and trading volumes now regularly compete with Ethereum and sometimes exceeds it despite having a fraction of the TVL (approximately $5.1 billion for Solana vs $47.6 billion for Ethereum). TVL represents dollars but not activity. Higher TVL does not necessarily equate to higher capital efficiency. That being said, TVL can provide a general indication of a chain’s economic growth trajectory. It can also be more capital intensive and harder to manipulate than other metrics such as volume or active addresses.

The table below shows Sui ranked at #12. While Sui still has a lot of ground to cover, it has real potential to compete with older and more established chains and make a move into the top 10. It is also growing faster than its older and direct competitor Aptos, which sits at rank #18 with approximately $415 million TVL.

Source: DefiLlama

Sui’s TVL grew strongly from the end of Q3 2023 to present, where TVL increased from around $50 million to $610 million. It reached a peak of $751 million in May 2024.

Source: DefiLlama

In the same time period, the amount of SUI increased from 105 million to 715 million, which demonstrates that the dollar value increase in the TVL has not been solely due to the price appreciation of SUI. More SUI is clearly participating in Sui ecosystem through things such as DeFi protocols.

Source: DefiLlama

Other Metrics

Transactions, Addresses, DEX Volumes

It is hard to get a complete and fair reading on the number of (1) daily transactions, (2) daily active addresses, or (3) daily DEX trading volumes, as there have been several inorganic spikes in activity since Sui launched which I cannot explain yet.10 However, outside of those anomalies, it is clear that metrics have at least gradually increased since Sui launched even if there has been a slump in activity over the past few months. There has been no noticeable and sustained decrease where those metrics continue to make new lows. It is early days though, so these metrics need continued watching.

Active Validators

The number of active validators on Sui has remained steady since mainnet launch, rising only slightly from 104 to 106.

In July 2024, Mysten Labs pushed the Mysticeti consensus upgrade from testnet to a phased mainnet rollout. Mysticeti significantly reduces latency and validator CPU requirements. This upgrade not only make the network more performant but will also hopefully increase Sui’s decentralisation by making it cheaper (and more sustainable) for anyone to run a validator on the network.

Ecosystem Projects

Wallets

Sui has a decent selection of native software (hot) wallets: Martian, Fewcha, Ethos, Suiet, Surf, and Sui Wallet, which I have assessed in the table below against some key considerations. In my view, outside of UX and UI, wallet security and privacy should be the paramount concern when choosing a wallet.

“zkLogin” is a Sui native feature where new users can create a wallet using common Web2 authentication and credentials from providers like Google, Meta, Microsoft, Apple and Twitch. zkLogin provides a more familiar and seamless sign up process, bypassing the traditional, high-friction requirement for users to manage and record private keys and seed phrases. It uses zero-knowledge proofs to create stable wallet addresses that have "zero knowledge" of the provider (like Google) or credentials (like email address) when those are options used, meaning no personal information live on-chain. I am not aware of any other chain that enshrines this type of feature at the base network level. If apps on other chains have a similar feature, the app and their users need to rely on third party authentication solutions, which introduces an extra level of trust and dependency.

If you want cold storage, Sui is also available with Ledger.

Wave Wallet is also attracting attention due to it being a Telegram-based wallet for Sui.

Other multi-chain software wallets have integrated Sui, such as Nightly, Trust Wallet, OKX Wallet and Bitget Wallet. However, I generally favour native wallets because you tend to experience a cleaner UX and UI, plus native wallet teams usually give more attention to wallet features catered specifically for the native chain.

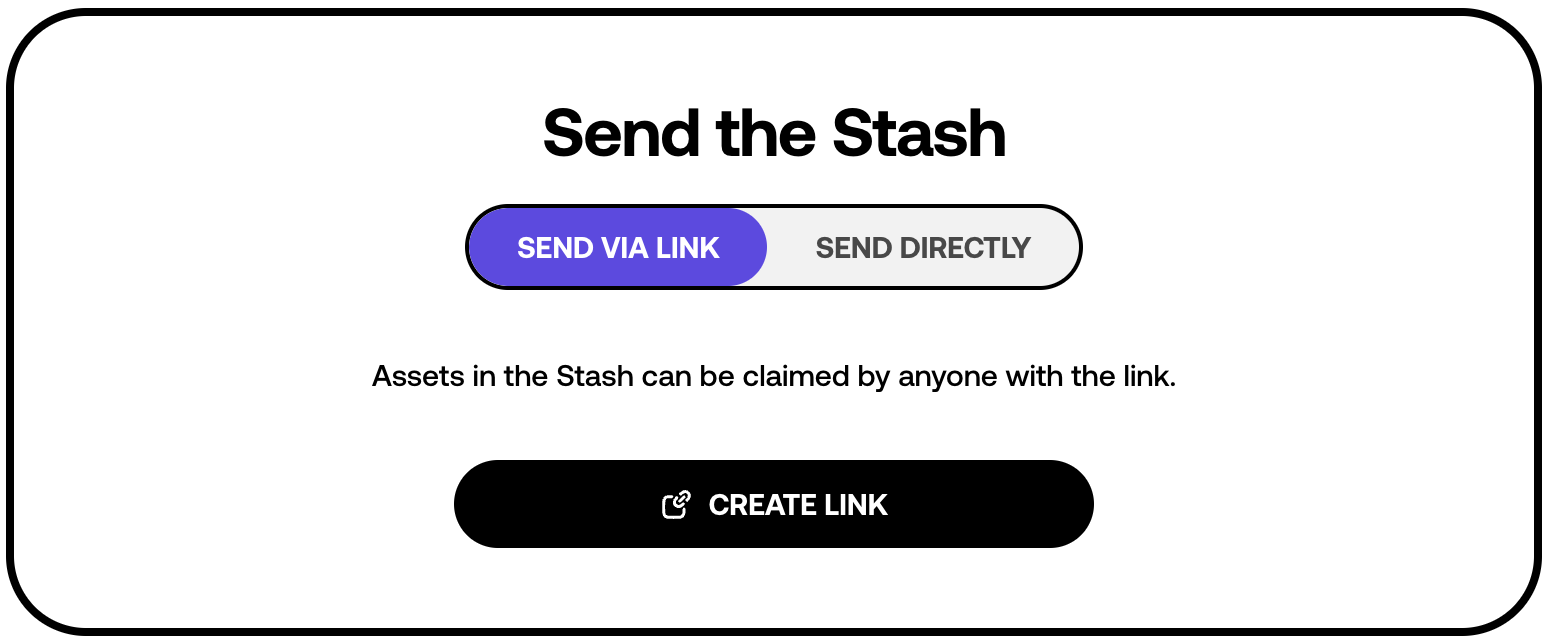

Stashed is a new product developed by Mysten Labs that allows users to send SUI, other Sui-based tokens and/or NFTs to others by generating a simple link. The recipient can claim the assets by clicking the link and signing up for a self-custody wallet using their Google or Twitch accounts. This process uses zkLogin.

DEXs

Sui has quickly formed a competitive DEX landscape.

Cetus is the leading DEX and liquidity protocol on Sui, utilising a CLMM model instead of the traditional AMM model. It is also available on Aptos. Aftermath is another DEX and liquidity protocol (allowing liquidity pools of up to 8 assets) sitting comfortably in second.

DeepBook is not a DEX but it has grown to become an important liquidity infrastructure protocol which Sui dApps (such as the other DEXs) can tap into.

Some smaller competitors are:

Kriya - a DEX and liquidity protocol (AMM + CLMM) that will expand to offer perpetual futures trading soon.

FlowX Finance - a DEX (and DEX Aggregator) that also offers liquidity portfolio management and a project launchpad.

Turbos Finance - a DEX and liquidity protocol (CLMM).

Hop is a DEX Aggregator similar to what Jupiter was early on. There are a lot more features that need to be added (e.g., Limit Orders, DCA) but I think it is currently the most convenient and user friendly option for swaps on Sui.

Derivatives / Perpetual Futures DEXs

BlueFin is the clear leader in Sui’s derivatives exchange market. It has facilitated over USD$33 billion in cumulative volume since its launch in May 2023, maintains a market share of well over 70% on Sui, and holds over USD$16 million in TVL, helped in part by its integration with Elixir.11 It expects to launch its governance token BLUE within a few weeks at least (it was originally scheduled for July 2024). BlueFin is one of the key projects on Sui to keep an eye on.

ABEx is another derivatives exchange on Sui but it has nowhere near the same traction as BlueFin in terms of liquidity, volume or mindshare.

Liquid Staking

Sui has two key Liquid Staking protocols: Volo (vSUI) and Haedal Protocol (haSUI). In addition to being a DEX, Aftermath also offers its own Liquid Staking Token (LST) called afSUI.

These protocols enable exposure to typical LSTs that you will find on most chains.

DeFi

Sui’s DeFi ecosystem is also steadily growing.

Navi is the clear leader with over $230 million TVL. It is an over collateralised lending and borrowing protocol that also offers leveraged yield strategies. Navi plans to go cross-chain in the near future, almost certainly with Aptos first.

Similar to Navi, Scallop and Suilend are the other major protocols in Sui’s lending and borrowing market with TVL over $110 million and $85 million, respectively. Scallop recently integrated with Solana. Suilend is a newer player from the same team behind Solend (now Save) on Solana, but has quickly grown due to its ongoing SUI incentives and Suilend Points campaigns.

Other notable DeFi protocols are:

Ondo Finance - already popular on seven chains including Ethereum, Solana and Mantle, Ondo’s USDY product has been steadily growing on Sui. USDY is a yield-bearing USD stablecoin backed by short term US Treasuries and bank demand deposits.

AlphaFi - automated yield aggregation strategies for dual-token liquidity pools and single sided lending.

Bucket Protocol - collateralised debt positions for its overcollateralised native USD stablecoin BUCK. Sparkling Finance is an additional product in the Bucket ecosystem, allowing BUCK to be staked in its fee-accruing staking pool and wrapped to sBUCK to become a yield-bearing stablecoin.

Typus Finance - variety of products including options, perpetual futures (soon), and onchain gambling games.

Strater - one-stop hub for DeFi strategies across many of Sui’s leading DeFi protocols.

NFTs

Sui’s NFT scene is very nascent at the same time that most NFTs are struggling across all chains, so I would not expect much activity or innovation for now. There are several established NFT marketplaces though.

TradePort is a trader-focused marketplace akin to Blur or Tensor. It is not native to Sui as it also operates on Stacks, Near and Aptos, but since launching on Sui it has quickly attracted a significant majority of the chain’s NFT trading volume.

Clutchy, BlueMove, and HyperSpace are traditional NFT marketplaces.

Other Apps

Sui Name Service is a typical domain service that lets users register human readable names (e.g. pashi.sui) for their Sui wallet addresses.

Pump Up from Double Up is essentially a clone of Solana’s pump.fun (both as a product and with its UI). Double Up caters not only to memecoins, but other casino games too. Hop, the DEX aggregator mentioned earlier, is also planning to launch a similar memecoin product. Considering pump.fun is regularly among the highest fee earning apps in the entire market, it is unsurprising that pump.fun clones are popping up on other chains. It is questionable whether these gambling focused apps or other hyper financialised crypto apps like Fantasy.top have long term futures. Even though a lot of retail activity in 2024 has been concentrated on memecoins, you only need to go to the comments section of recent pump.fun posts to realise retail sentiment is shifting to viewing these products as being a net negative. Some interesting experimentation has occurred around these apps but hopefully the overall success of a crypto native app will inspire builders to create other innovative crypto native apps that can compete for a similar level of attention but are less hyper financialised.

Conclusion

I think Sui is worth paying attention to closely. It has differentiated itself from the countless other Layer 1s with the Move VM and programming language. It has also attracted more builders and liquidity than its direct competitor Aptos, and maintained gradual and steady growth in its DeFi ecosystem. I am not making any absolute statement about its prospects of success but these are all positive early signs. That being said, market conditions have been more favourable over the past 12 months. Sui will inevitably face its toughest but necessary battle when conditions turn bearish over an extended period (whenever and for however long that might be). If users, developers and (ideally) capital largely stay and continue to use, build and innovate even when the native currency’s price collapses or liquidity or volume dries up, this can be a strong sign of an ecosystem with much brighter days ahead. It happened with Ethereum after 2017 and it happened with Solana after 2022.

Over a longer time horizon, it is possible that neither Sui, Aptos or M2 (Movement Labs’ Ethereum Layer 2) achieve escape velocity with adoption. Instead, it may be that only the Move VM and language gains accelerated adoption as implemented by other projects yet to come.

While Bitcoin seems destined to retain relevance as digital gold / store of value long into the future, it is very possible Ethereum and Solana will be overtaken by other blockchains that may not even exist yet. Nobody should be complacent about this possibility.

For the purpose of this commentary I’m ignoring Layer 2 Rollups like Arbitrum, Optimism, Base or Blast and EVM-compatible Sidechains like Polygon PoS because they do not strictly qualify as independent Layer 1s.

The Total Value Locked on TON grew from approximately $20million USD at the beginning of March 2024 to around $350 million USD today: see DefiLlama. There has also been significant growth of users, transactions and onchain trading volume: see Dune dashboard by @nyssarex and The Block.

I would like to see more consumer app focused crypto funds launch soon. Paradigm recently announced it had raised a third $850 million USD fund which will focus on “crypto projects at the earliest stages”. It is expected Paradigm will use this fund to focus on apps more, but it doesn’t appear precluded from investing in more infrastructure projects too.

For Ethereum Layer 2s, MegaEth has caught my eye. Hyperliquid is also interesting as its small, fast-shipping team has grown a strong community and has not received any VC funding. However, its custom L1 needs to offer users other innovative financial applications other than just a spot and Perpetual DEX with Vaults, so I’m reserving further judgement until more plans and projects are announced and launched. It will be worth analysing Hyperliquid’s user and liquidity retention rate in the months following its token airdrop (likely Q4 2024).

See, for example this article by Placeholder.

For a helpful discussion on this recent dilemma between public valuation and private capture, see this article by Cobie.

See also: Sui Vision Statistics.